The Simpson-Bowles deficit commission recommendations (pdf) have raised a sort of philosophical question for free-marketers: do so-called “tax expenditures” count as government spending?

Tax expenditures are preferences, deductions, credits, and loopholes in the tax code that allow targeted groups, products, or activities to avoid taxation. For example, the tax revenues forgone because of the tax exemption for employer-provided health insurance, the mortgage interest deduction, and the state and local tax deductions are all examples of tax expenditures. The Simpson-Bowles plan would eliminate or reduce many of these deductions and use the revenues to lower marginal income tax rates — with a little revenue left over to reduce the deficit.

There is a question whether the revenues raised from eliminating tax expenditures should count as tax increases or spending cuts. Josh Barro, at NRO, argued that tax expenditures are indeed spending, and thinks that the Simpson-Bowles cuts are a good idea. The folks at the Cato Institute, however, have a different idea: tax expenditures should not be cut unless “every penny” of the revenue raised goes toward lowering tax rates. Dan Mitchell writes:

The bad news is that [the Simpson-Bowles measures would] result in more revenue going to Washington. In other words, the tax increase resulting from fewer tax distortions is larger than the tax decrease resulting from lower tax rates. To put it bluntly, the plans would increase the overall tax burden.

And in the Wall Street Journal a few days ago, Stephen Moore and Richard Vedder made a similar point, namely that increased revenues always means more spending, as opposed to less debt. According to their research, “over the entire post World War II era through 2009 each dollar of new tax revenue was associated with $1.17 of new spending. Politicians spend the money as fast as it comes in–and a little bit more.”

Mitchell goes a step further and says that, because extra revenues yield increased spending, getting revenues from eliminating tax expenditures would actually make balancing the budget harder than otherwise. He produces this graph, generated from CBO data, to reinforce his point that simply curtailing spending is enough to balance the budget, even including extending the Bush tax cuts:

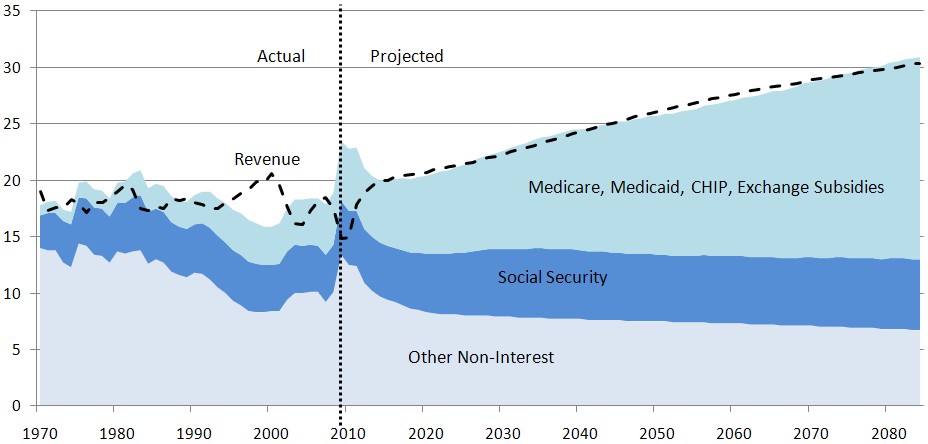

While there is a real tactical logic to opposing any tax hikes/revenue increases, there is a limit to this line of reasoning. That limit becomes apparent when you extend the budget graph past 2020, and show the components of spending. Austin Frakt has done just that:

It should be clear from this graph that the real threat to the nation’s fiscal solvency is not just the near-term primary budget that Mitchell’s looking at, but the long-term rising cost of health care entitlements, and the service on the debt that will be needed to finance those entitlements

One major driver of health care cost inflation is the tax exemption for employer-provided health insurance. Frakt estimates that this wrinkle in the tax code leads Americans with employer-provided health insurance to spend 26 percent more than they would without the tax benefit. That overspending, in turn, puts inflationary pressure on health care products and services, raising the costs for everyone

So the problem with the tax expenditure on employer-provided health insurance is not just forgone revenue. The exemption also exacerbates the biggest fiscal problem we face, namely health care cost inflation.

The other big-ticket tax expenditure items have similarly harmful secondary effects. For example, it could easily be argued that the mortgage tax deduction played a role in the housing market boom and bust.

Those unintended effects should be taken into consideration when talking about tax expenditures, whether eliminating them would be cutting spending or raising taxes.